The Opportunity in Canada’s Mid-Market Apartment Sector

Key Takeaways:

- ‘Mid-market’ apartments are purpose-built rental buildings with wide renter demand and attainability. These buildings are typically older and priced within the second and third quartile of rents within their respective markets. Attractive asset pricing, emerging liquidity and strong income growth potential are creating compelling sector opportunities for investors.

- The case for mid-market residential is driven in part by the depth of its renter pool and the associated resilience of its demand profile. Its price point and market positioning make it attractive to a diversity of renter cohorts and income groups, adding to its stability through cycles.

- With strong market rent growth and limited turnover in recent years, asking rents remain well above in-place rents for mid-market apartments. This is creating accretive ‘mark to market’ rent effects with income growth opportunities for investors.

- Another opportunity for investors is improving the quality of mid-market housing through building, energy and in-unit upgrades. Nearly 80% of the existing rental inventory in Canada is more than 25-years in age, most of which remains under-invested and under-capitalized.

- Our estimate is that more than half of the purpose-built rental inventory nationally (an estimated 1.3 million units) can be characterized as mid-market, creating a wide opportunity set for investors across Canadian markets.

Amidst shifts in multi-family market conditions, compelling investment opportunities are emerging in the ‘mid-market’ segment of the residential rental market—characterized as legacy apartment buildings with resilient demand and affordability.

Rental apartment buildings have long-been a key part of property investor’s portfolios, with structural demand, limited supply and stable cashflows defining features of the asset class. Indeed, multi-family has been among the most resilient property sectors in Canada, providing investors 6.8% annual total returns and 3.3% annual income growth over the long-term. [1]

The residential sector is not a monolith however, and shifts in market conditions are driving the case for more tactical approaches to the asset class. Where we see strong opportunity is in the ‘mid-market’ segment of the residential market, defined in our view as existing, typically older rental apartment buildings attainable and attractive to a wide range of occupiers. Demographic tailwinds, income growth potential and structural elements unique to the segment combine to provide a compelling entry for investors.

Sizing the Mid-market Opportunity

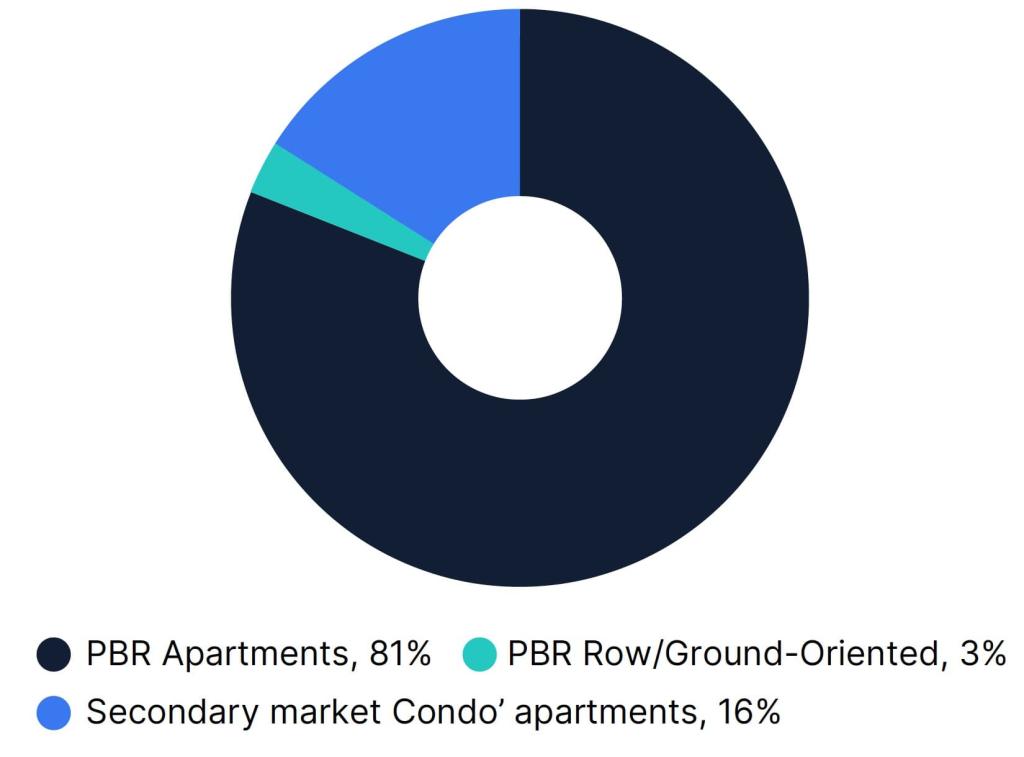

According to the Canada Mortgage and Housing Corporation (CMHC), there are an estimated 2.9 million rental units across Canada, of which, 81% or 2.3 million units are within purpose-built rental apartment buildings [2] . Despite significant growth in the secondary ‘condominium’ rental market and other housing formats the last several decades, purpose-built rental remains the largest component of rental housing nationally (Figure 1).

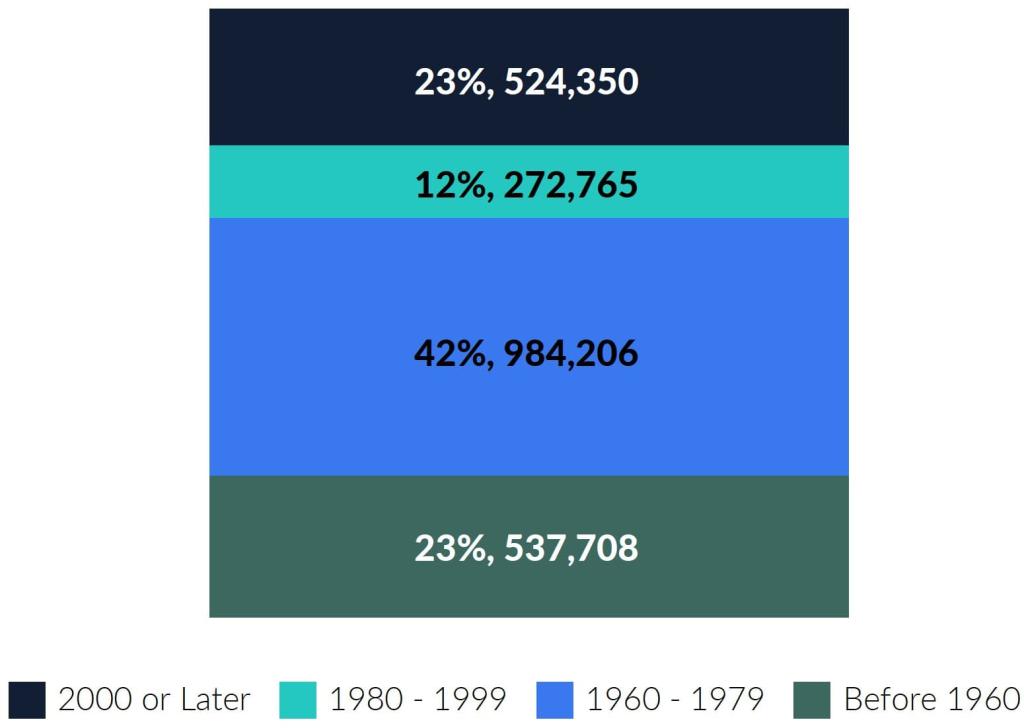

Within this purpose-built inventory, close to 80% are in buildings more than 25-years in age. Segmented data further shows most of the rental apartment inventory in Canada are in buildings more than 45 years in age (Figure 2). Although there has been sizable delivery of new purpose-built apartments in recent years (218,000 units, or 9.4% of today’s inventory was built the last three years), most is of a prior vintage.

It is within this existing apartment stock from where we derive our mid-market opportunity. Our estimate is that more than half of the existing rental inventory can be classified as ‘mid-market’ based on one or more of the following characteristics:

- More than 25 years in age but are functional and in good quality

- Within the second and third quartile of the market based on average asking rents

- Attracts and is occupied by a wide segment of renter households and incomes

Through this definition of mid-market, new rental inventory (an estimated 10-20% of the purpose-built rental inventory) is excluded due to the focus on a narrower and higher segment of renter incomes. Conversely, we also exclude what we define as ‘core-housing’ stock (estimated 20% of the purpose-built inventory on the opposite end of the spectrum) that serves the affordability segment of the market and with a different ownership and operating profile.

A majority of rental stock is in purpose-built rental (PBR) buildings

Figure 1: Canada rental inventory by type (units)

(Source: CMHC Housing Market Information Portal, Q4 2024)

Lack of new supply means most of Canada’s purpose-built rental stock was built more than 25 years ago

Figure 2: Canada’s purpose-built rental apartment stock by age of construction (units)

(Source: CMHC Housing Market Information Portal, Q4 2024)

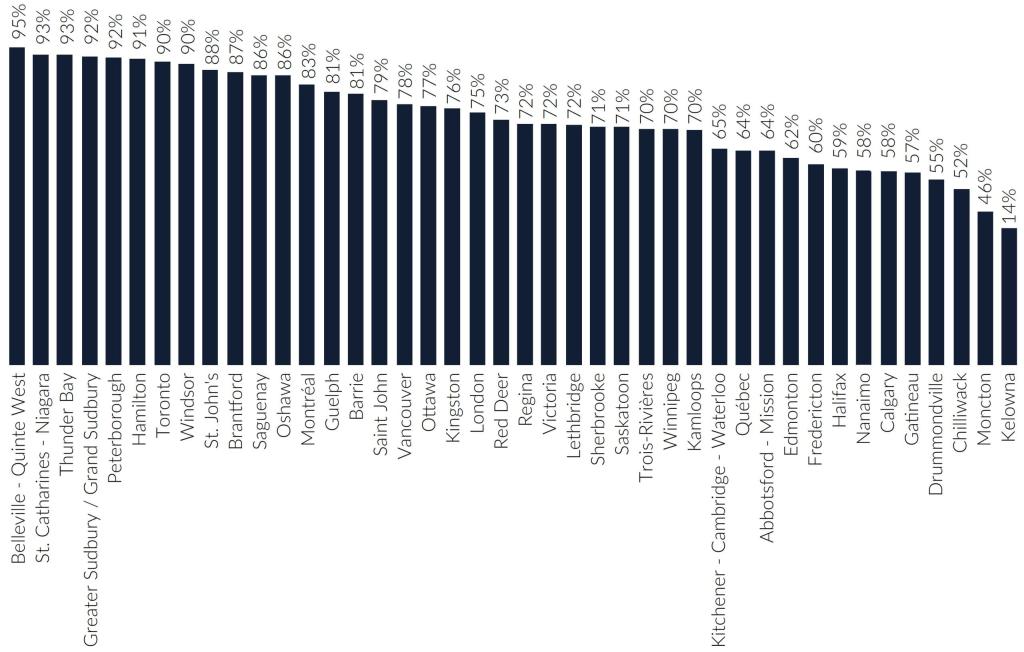

Mid-market opportunities exist across all major markets

Figure 3: Share of purpose-built rental apartment inventory (units) built before 2000 – by major Census Metropolitan Area (CMA)

(Source: CMHC Housing Market Information Portal, Q4 2024)

The Case for Mid-Market Residential

Resilient Demand

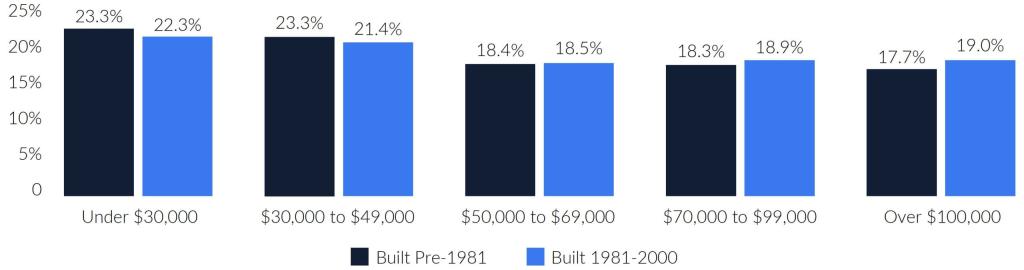

The case for mid-market residential is driven in part from its resilient demand profile. The sector’s balance between price point, affordability and quality attracts a diverse renter base and adds to the sector’s stability through cycles. Data shows a broad range of income groups occupy buildings in the segment (Figure 4).

This wide attainability means mid-market residential also draws from a large cross-section of existing renters in a market. This includes for instance those ‘moving-up’ in quality from their existing homes or those ‘moving-down’ whether for size, lifestyle or cost reasons. Rising homeownership costs are another factor supporting growing rental demand in the mid-market segment—elevated interest rates and home prices continue to support a rising share of renter households nationally, namely those looking for more accessible price points [3] . Notably, a growing cohort of high-income renters occupy mid-market inventory in Canada—nearly one-fifth of mid-market stock is occupied by households with incomes of $100,000 or more (Figure 4).

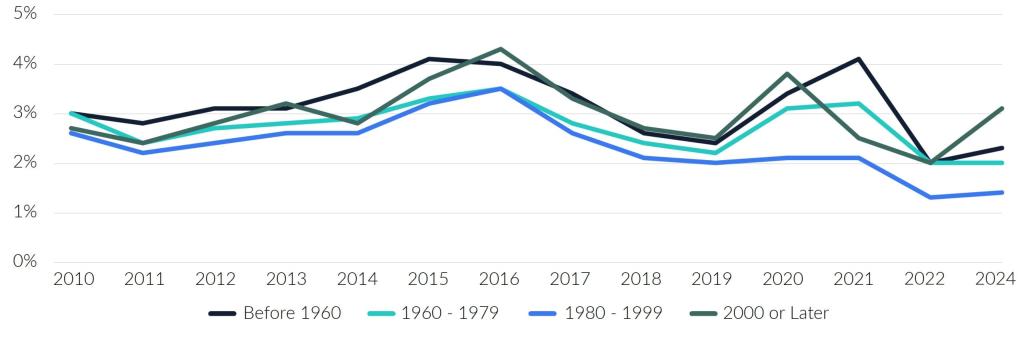

This resilience is a driving point for performance today; after record population growth through the post-covid (2021-2023) period, recent changes to immigration policy have generally sought to temper international migration and move population growth to more sustainable levels [4] . These changes have had varied effects across the multi-family rental market through 2025; mid-market residential has largely been resilient based on the aforementioned factors (Figure 5 and 6). Sectors with a narrower and higher-income demand profile—namely new rental construction and higher-priced condo rental units—have seen moderating demand as pent-up conditions have eased.

A wide cross-section of renter profiles occupy older rental inventory

Figure 4: Distribution of renters by household income and building vintage

(Source: Statistics Canada, 2021 Census, largest 13 CMAs. Segmented data for pre-1981 not available)

Mid-market rental seeing resilient demand relative to newer and higher-priced segments

Figure 5: Canada purpose-built apartment vacancy rate (%) by age

(Source: CHMC Housing Market Information Portal, Q4 2024 - no data available for 2023)

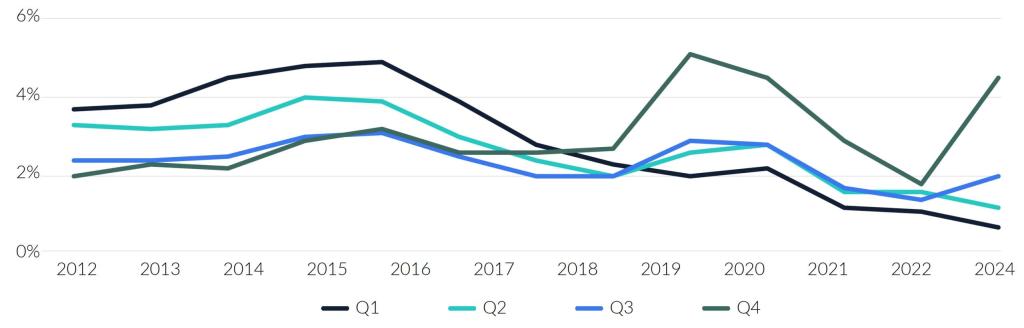

Vacancy levels segmented across price points

Figure 6: Canada purpose-built apartment vacancy rate (%) by rent quartile

(Q4 = Highest Rent, Q1 = Lowest Rent)

(Source: CHMC Housing Market Information Portal - no data available for 2023)

Attractive Income Growth Potential

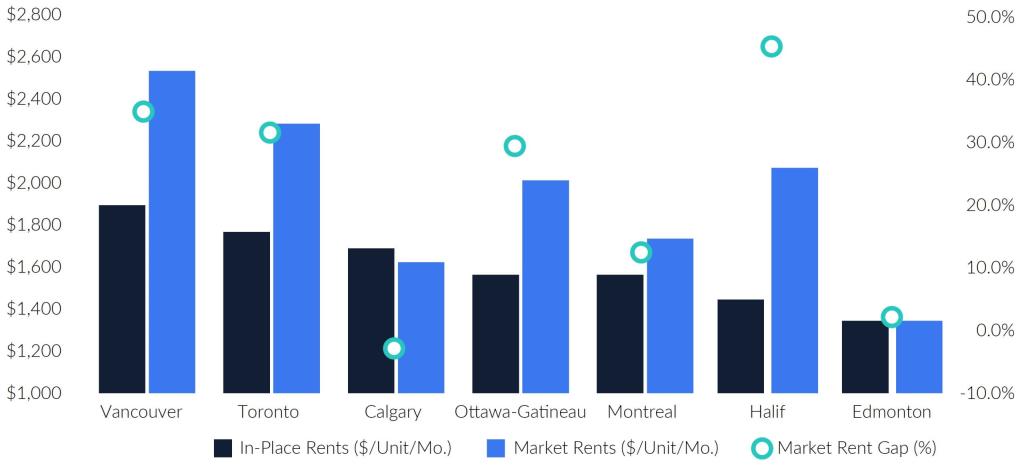

A confluence of strong market rental growth, limited tenant mobility and low vacancy the last several years have led to cyclically high spreads between in-place and market rents for mid-market inventory (Figure 7). It is this ‘mark to market’ opportunity that presents compelling opportunities for income growth. When a unit turns over, rents reset to market, and increases in achieved rent translate to income growth.

When we look across major markets in Canada, the in-place rent gap to market varies. Some markets such as Toronto, Vancouver, Ottawa and Halifax have sizable in-place to market spreads of 30-45%, contrast to Calgary, Edmonton and Montreal where the gap is in the 0-10% range.

The variance across markets depends on several factors, including average turnover rates, prior market rent growth, alongside jurisdictional differences and approaches to rent control. In markets with smaller in-place to market rent spreads, mark-to-market opportunities will likely vary

by property and across/within sub-markets.

Notably, data suggests turnover rates have started to increase across Canadian markets, a result of more balanced demand-supply conditions as demographic pressures ease [5] . This increase in tenant mobility further supports strong income growth potential as mark to market opportunities are unlocked at an elevated pace.

Mark to market opportunities within older rental inventory

Figure 7: Estimated market and in-place rents, 1-beds, major Canadian CMAs ($/Unit/Month), as of Q2 2025

(Source: GWLRA, Yardi, Rentals.ca)

Improvement Opportunities

Much of the mid-market rental stock in Canada is unimproved and, in many cases, under-invested and under-capitalized. This presents an opportunity to improve the quality of mid-market rental housing nationally through upgrades such as modern finishes and improved layouts in units, alongside strategic investments in building amenities and infrastructure. We see rental units positioned between new/luxury offerings and old/unimproved inventory as filling a critical gap in the housing market today. While various government programs and incentives have supported development of mid-market rental offerings in recent years, it remains limited on an aggregate basis.

Growing regulatory requirements and stakeholder input is also pushing the need for stronger energy efficiency within existing rental buildings, another area where capital can and should be invested. This includes conservation programs and building automation, utility and mechanical system upgrades targeting water, waste and energy (‘WWE’) reduction. In our buildings with active capital programs, we are seeing meaningful energy reductions being realized, leading to lower utility costs and pass through effects for occupants.

Entry Points

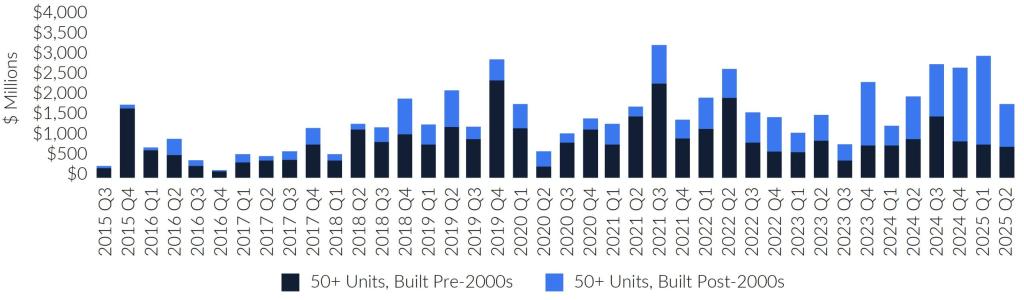

After reaching cyclical lows through 2023, transaction volumes for multi-family rental assets have rebounded the last 18 months and are trending near historical averages (Figure 8). Stability in interest rates and inflation, alongside stable cash flows and available financing for residential assets have been factors supporting renewed deal volume the last several quarters. Overall, $6 billion (B) of multi-family assets are traded annually on average in Canada, within some years exceeding $8B-$10B in total. Buildings built before 2000 make up 60-70% of multi-family asset purchases annually. This broader volume of deal flow and liquidity continues to provide attractive entry points for mid-market investors.

Reflective of a broader re-pricing across private real estate, capitalization (cap) rates for multi-family rental properties have also risen 50-75 basis points from historical lows with yields for older properties 25-50 bps higher than newer buildings (Figure 9). Current property yields are also at near decade highs, providing a unique time to realize strong return and cyclical value opportunities.

National multi-family transaction volumes rebounding

Figure 8: National quarterly multi-family property investment volumes ($ Millions)

(Source: CoStar - denotes assets with +50 units)

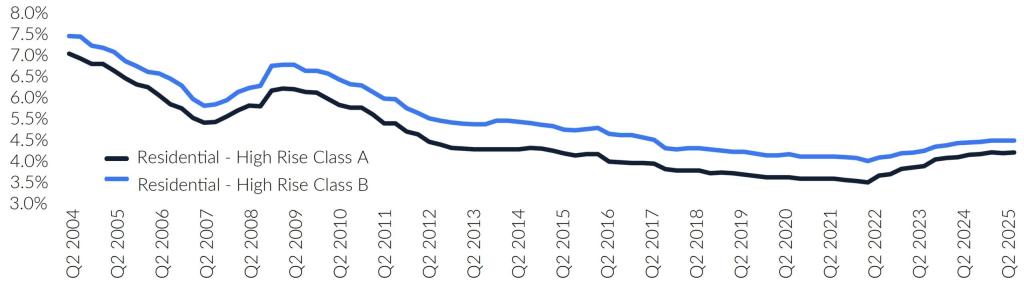

Shifts in property yields creating value opportunities

Figure 9: Residential cap rates - national Canadian average

(Source: CBRE)

Conclusion

Mid-market assets provide a unique opportunity for investors today given cyclical upside in performance anchored by structural demand. The ability to improve mid-market assets to meet shifting market demand is another attraction point as affordability and sustainability remain

top of mind among owners and occupiers alike.

Source: MSCI Canada Direct Property Index (as of Q2 2025), 10-year average annualized total returns and net operating income growth.

Source: CMHC annual Rental Market Survey (Q4 2024). Privately initiated purpose-built structures containing 3 or more rental units. CMHC does not publish a single, national total for the number of rental apartment buildings in Canada, but instead segments units based on building type and size, year of construction, and geography.

See Proof Point: Is Canada becoming a nation of renters? - RBC for more information.

See https://thoughtleadership.cibc.com/article/population-growth-projections-are-we-repeating-past-mistakes/ and https://thoughtleadership.cibc.com/article/are-new-immigration-targets-really-an-economic-gamechanger/ for more information.

Source: CMHC 2025 Mid-year Rental Market Update, Yardi Q3 2025 National Multi-family market report.

Contact

Anthio Yuen

Vice-President, Investment Strategy & Product Development

anthio.yuen@gwlra.com

Simon Lo

Vice-President, Portfolio Management

simon.lo@gwlra.com

Craig Hatt

Senior Director, National Multi-family Asset Management

craig.hatt@gwlra.com

This report is for general information purposes only and is not intended to provide any personalized financial, investment, real estate, legal, accounting, tax, medical or other professional advice. While the information contained in this report is believed to be reliable and accurate at the time of posting, GWL Realty Advisors Inc. and its affiliates (“GWLRA”) does not guarantee, represent or warrant that the information contained on this website is accurate, complete, reliable, verified, error-free or fit for any purpose. No endorsement or approval of any third party or their statements, opinions, information, products, or services is expressed or implied by the contents of this report.

GWLRA expressly disclaims all representations, warranties or conditions, express or implied, statutory or otherwise, including, without limitation, the warranties and conditions of merchantable quality and fitness for a particular purpose, non-infringement, compatibility, timeliness, security or accuracy. The user assumes full responsibility for risk of loss of any nature whatsoever resulting from the use of this report. For more information concerning the terms and conditions of use of this report, please refer to our website at https://www.gwlrealtyadvisors.com/general-disclaimer.

GWL Realty Advisors Inc. generates value by creating vibrant, sustainable communities that engage, excite and inspire. As a leading Canadian real estate investment advisor, we offer asset management, property management, development and specialized advisory services to pension funds and institutional clients. Our diverse portfolio includes residential, industrial, retail and office properties as well as an active pipeline of new development projects.