2026 Real Estate Market Perspectives: On the Cusp

Executive Summary

- Canadian private real estate enters the mid-point of 2026 at an inflection point. Improving capital markets contrast emerging economic and demographic risks and divergence within property sectors. “Bottom-up” strategies, namely a focus on income growth, asset selection and regional differentiation will be important for investors.

- Following increases in interest rates in recent years, private real estate has seen notable re-pricing, setting up for cyclical value opportunities looking forward. Property capitalization (“Cap”) rates are at 15-year highs, with underlying spreads to risk-free rates back to historical averages.

- Wide variation in market fundamentals continue to persist within property sectors. This bifurcation has heightened the importance of asset selection in performance generation, with greater consideration of property sub-sectors and site-specific characteristics.

- Property investment activity continues to improve relative to 2023/2024 lows. Large portfolio and entity‑level deals, however, have been notable contributors to the recovery alongside improvement in purchases of standalone properties. Investor demand remains strongest for assets with resilient income.

- Slowing population growth—primarily driven by changes in immigration policy—is expected to increase economic divergence across city regions. With fewer net new entrants to Canada in the near-term, competition for talent and people will intensify, further widening performance differences between regions.

Introduction

Contrasting forces are expected to shape private real estate over the near-term. On one hand, recent re-pricing of assets has improved return expectations, supporting a more active capital markets environment. On the other, several factors challenge the stability of market fundamentals, including ongoing economic and demographic risks and segmented fundamentals across property sectors.

Notably, these opposing forces parallel core drivers of real estate performance: total returns for real estate are largely a combination of 1) income return (influenced accordingly by economic growth), and 2) capital value growth (influenced accordingly by capital markets). Across cycles, the two forces complement or contrast to generate returns for investors. The onset of COVID for instance, saw robust capital markets support asset values as occupancy and cashflows were impaired. In more recent years, strong income growth served as an important hedge to rising interest rates and inflation. This duality is perhaps private real estate’s most enduring characteristic; opportunities for both cashflow and value growth over time, supported by structural stability.

In this Research Note, we outline key themes shaping our investment views and strategies across Canadian private real estate. Ultimately, investors are expected to face a competitive marketplace looking forward; a focus on income growth, asset selection and structural market opportunities will be important.

Theme 1

Convergence In Property Returns Signal A New Cycle

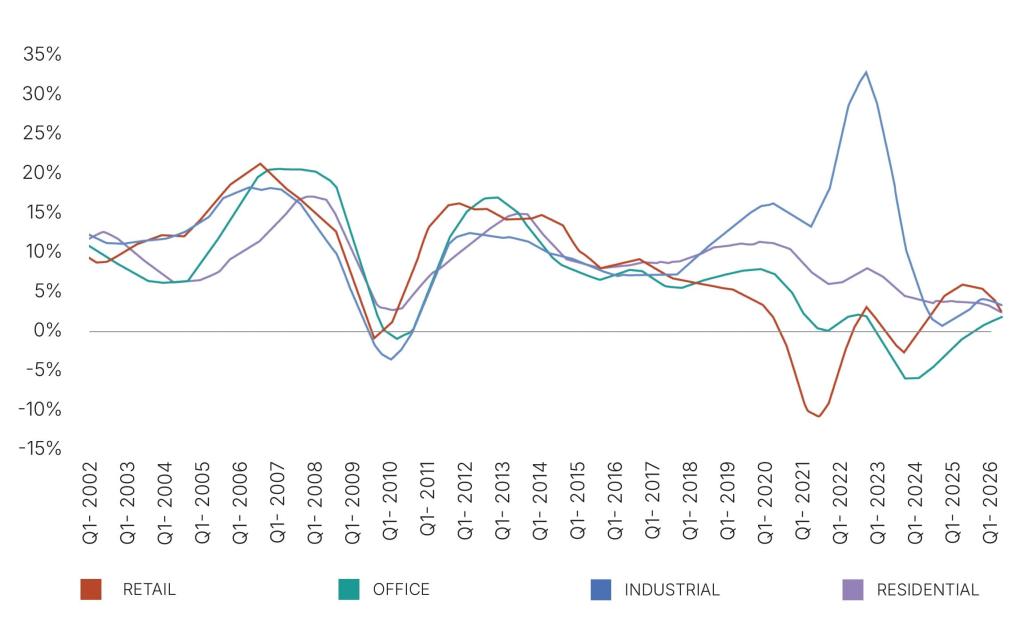

Over the past 24 months, total returns across property sectors have come together after several years of divergence (Figure 1). Stabilizing rent and income, and deceleration in capital growth have been key factors.

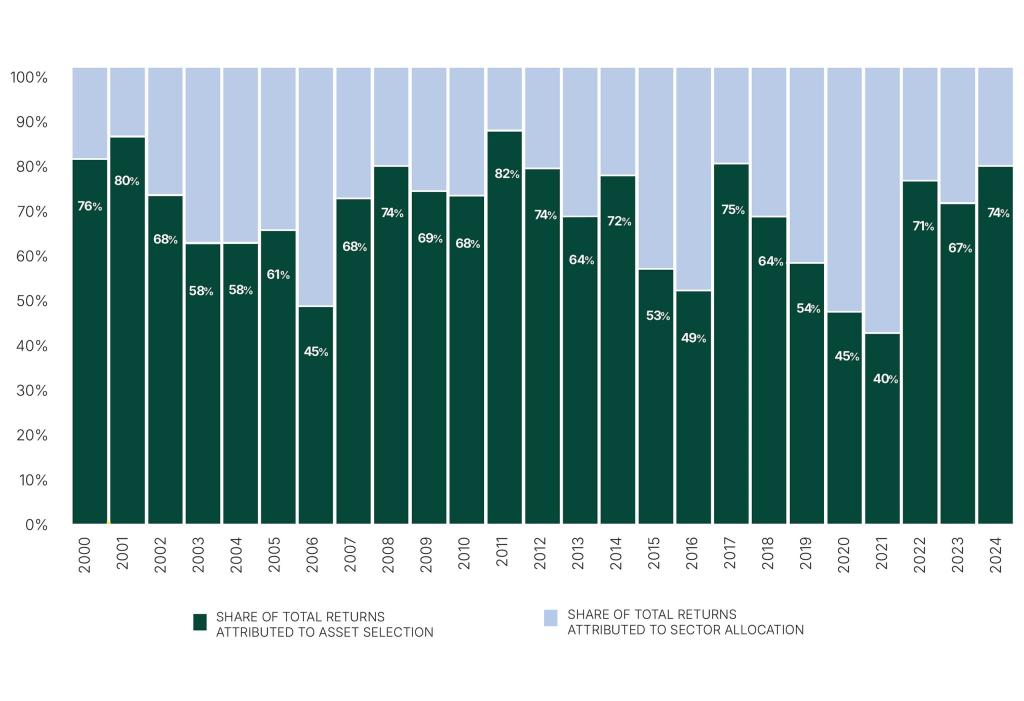

When we look historically, times of convergence have provided an important ‘reset’ cyclically. As for implications, asset selection will likely emerge as a driver of outperformance near-term as income returns anchor performance. Data from MSCI [1] shows that asset selection has a stronger influence on returns during periods of return convergence; sector allocation remains important, but the ability to drive ‘alpha’ is intuitively more pronounced when property sectors are in a divergent state (Figure 2).

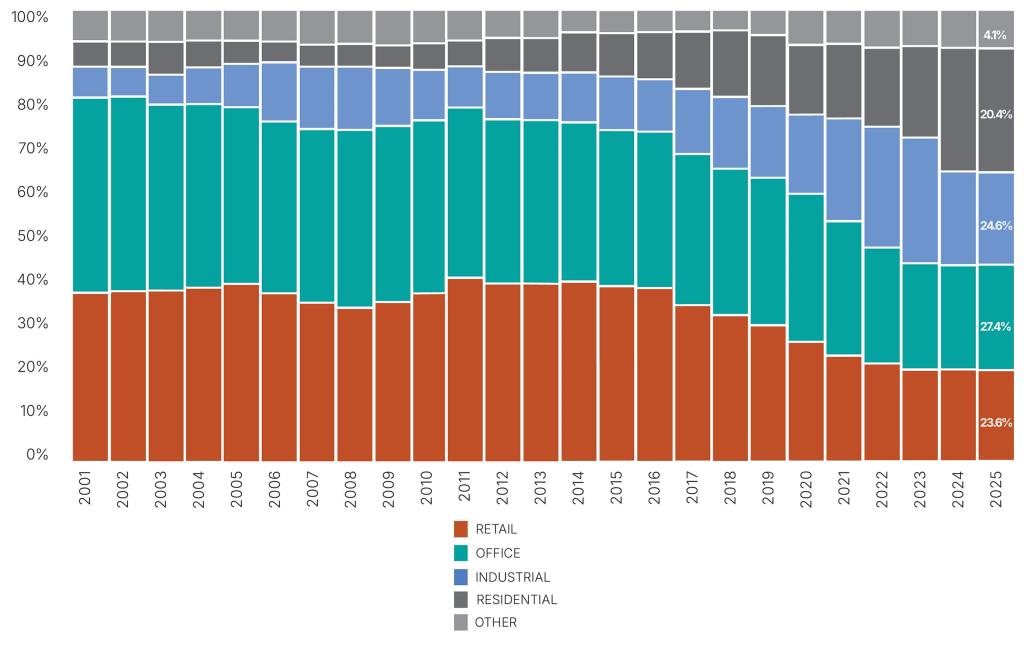

With this convergence, sector weights within the MSCI Canada Direct Property Index has also become more balanced. For the first time since the Index’s inception, major property sectors are represented in roughly equal proportions (Figure 3). Notably, the “other” category has also grown, reflecting increased institutional interest in alternative property types such as self storage, student housing, and life sciences facilities, among others. For investors with multi-asset portfolios, this ‘leveling-out’ in sector weightings provides an opportunity to revisit current sector allocation targets as new structural and cyclical trends emerge.

Across Major Property Sectors, Total Returns Have Converged

Figure 1: Annualized Private Real Estate Total Returns by Sector (Source: MSCI Canada Direct Property Index, Standing Investments)

Decomposing Private Real Estate Returns Show Impacts Of Asset Selection And Sector Allocation Cyclically

Figure 2: Annual Property Return Attribution for Direct Real Estate (Source: MSCI Canada Direct Property Index - all assets)

For The First Time, Private Real Estate Indices Are Balanced Across Major Property Sectors

Figure 3: MSCI Canada Direct Property Index, Share of Index Weight by Sector (Based on aggregate property value)

Theme 2

Property Prices Have Reset

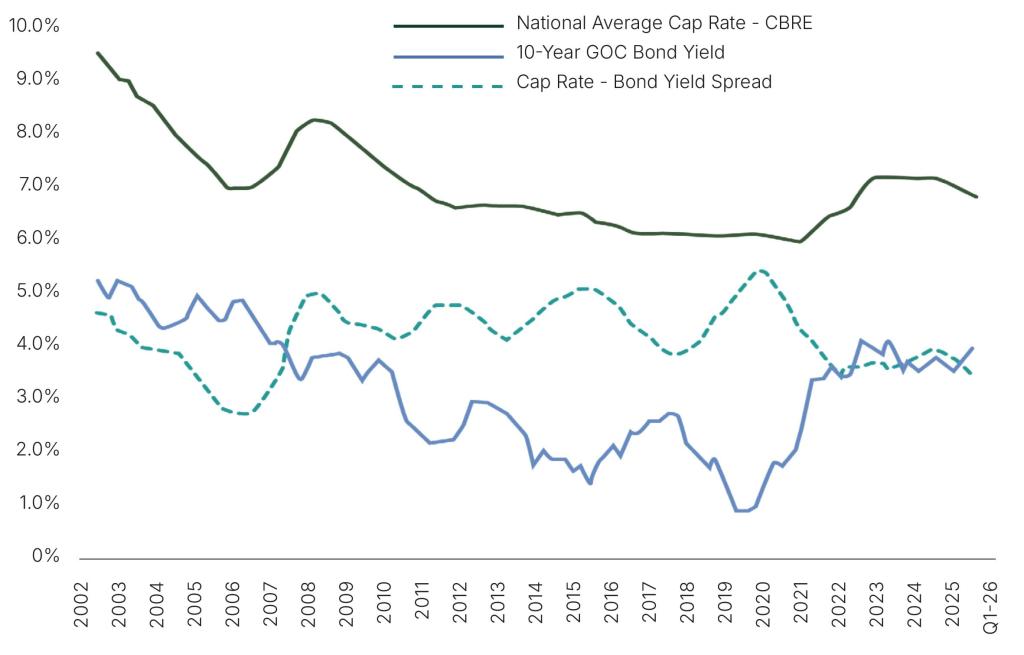

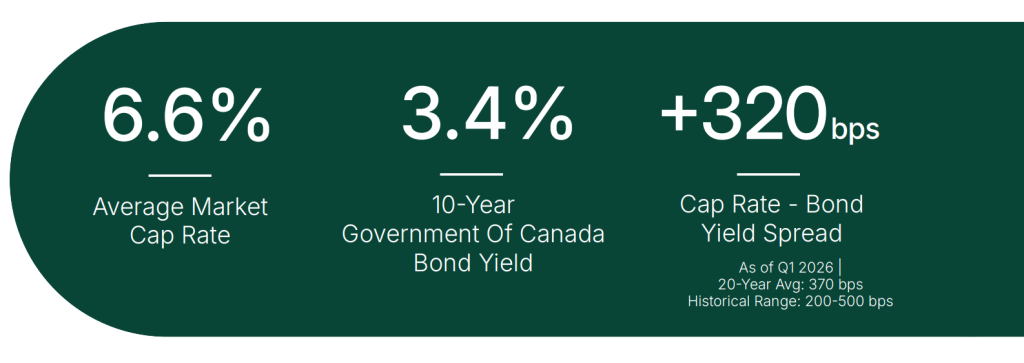

Following increases in interest rates in recent years, private real estate has seen notable re-pricing, setting up for cyclical value opportunities looking forward. After moving to post-COVID lows in 2023, property income returns (capitalization rates) have risen by approximately 120 basis points (bps) and now stand at 15-year highs.

Naturally, ongoing global conflicts add uncertainty as higher energy prices risk renewed upward pressure on inflation and interest rates. Despite this backdrop, current cap rates remain attractive on both an absolute and relative basis; when compared with long term interest rates, property cap rates offer an approximately 320 bps spread over 10-year Government of Canada bond yields, compared with a long term average of roughly 370 bps and a historical range of 200–500 bps. In addition, private real estate has historically provided a hedge against inflation, with contractual lease structures and rent escalations supporting resilient income growth and contributing to valuation stability over time.

Beyond attractive income returns, existing asset values remain below replacement cost—currently estimated at 10–20% depending on market and property type—highlighting attractive value relative to new development. Ongoing cost pressures are expected to keep construction starts low, further strengthening the appeal of income-producing assets near-term.

Property Cap Rates Are Back To 2011 Levels Providing Strong Income Return Opportunities

Figure 4: Property Cap Rate Spreads to 10-Year GOC Bond Yield (Source: CBRE, Oxford Economics)

Theme 3

Within Property Sectors, Market Fundamentals Are Bifurcated

In terms of market fundamentals, a closer look shows notable divergences occurring within each of the major asset classes.

Office | A Flight To Quality Trend

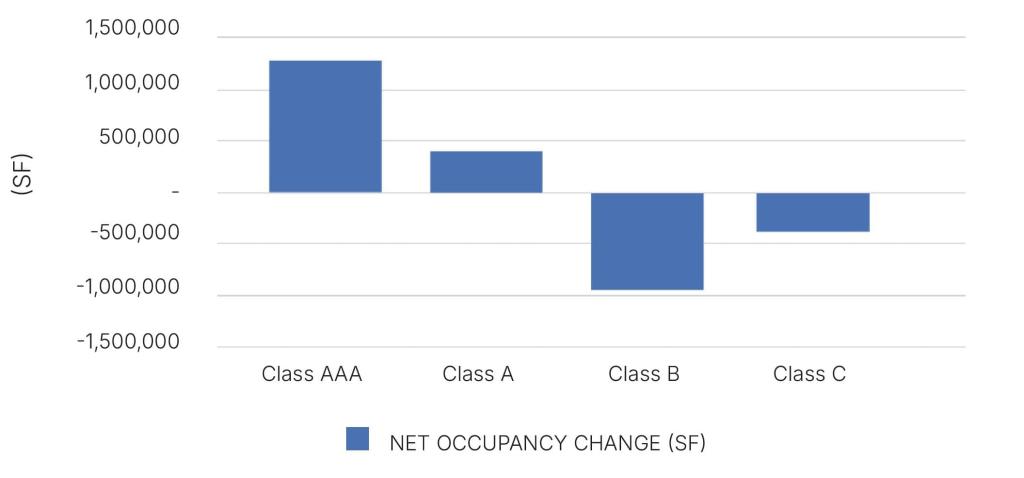

Market fundamentals in the office sector remain segmented by amenity profile and building vintage, with top-tier assets continuing to outperform. Across major office markets, a smaller subset of buildings—mainly existing and recently built ‘Class A’ properties offering strong amenities, transit accessibility, and modern specifications—have accounted for most of the market absorption the last several years.

Quality And Amenities Continue To Bifurcate Office Occupancy

Figure 5: Downtown Toronto: Office Net Occupancy Change (2022-25) (Source: CBRE)

Industrial | Vacancy Elevated Among New Supply

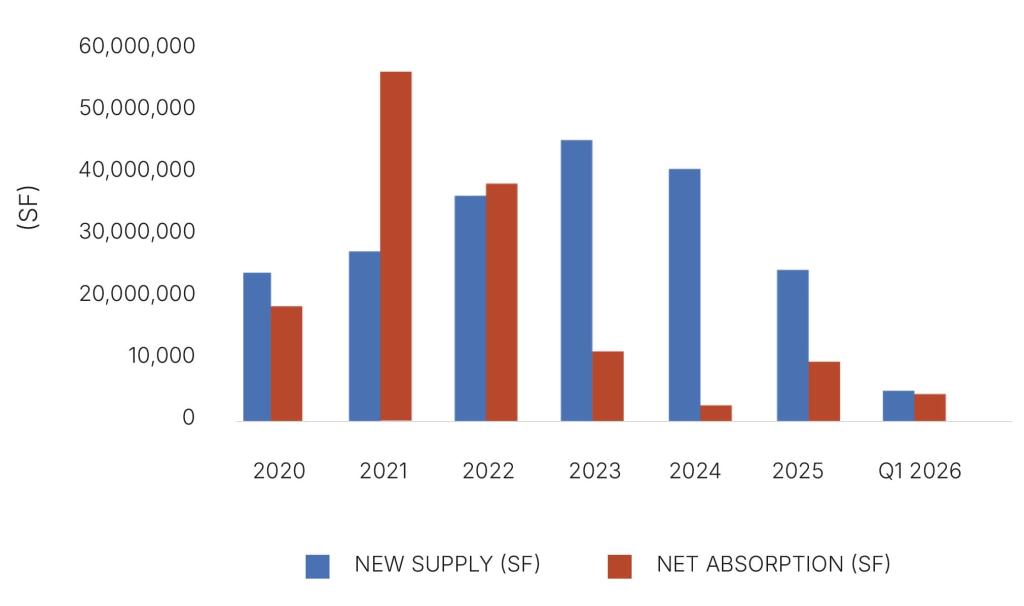

Among stable market conditions nationally, elevated vacancy persists for newer, recently built buildings. This reflects a re-balancing of supply and demand conditions after years of supply scarcity, with newly built assets leasing at a more measured pace than in prior years. In contrast, existing properties—especially those with a diversified and domestically-oriented tenant base—are performing well.

Supply Has Outpaced Demand Within Industrial In Recent Years, Though The Balance Is Improving

Figure 6: National Annual Industrial Absorption and Supply (Source: CBRE)

Residential | Cost Driving Divergence

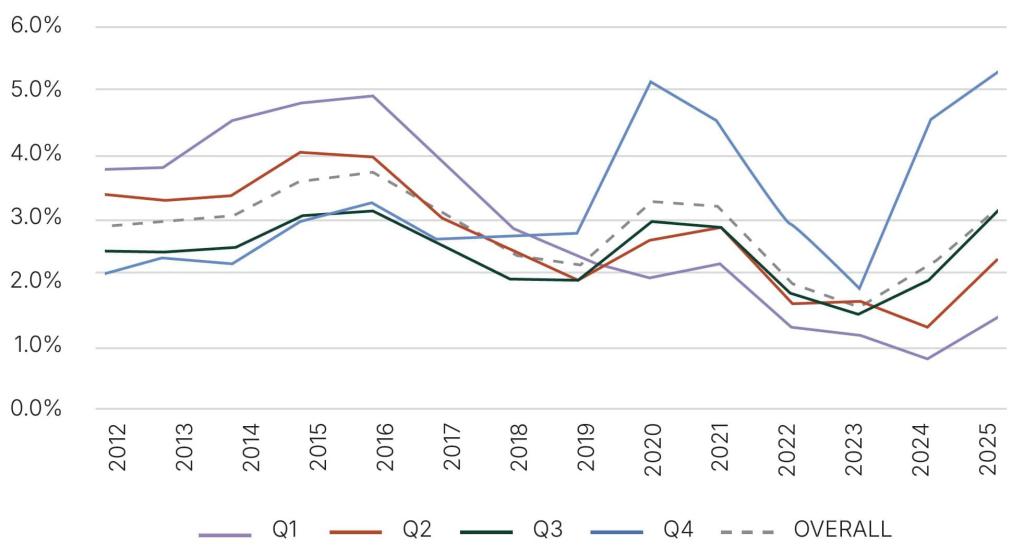

Reflective of ongoing pressures on housing costs, residential properties remain more divided by price point than by location or amenities. Multi-family segments catering to a broad renter income spectrum—particularly the mid‑market—have outperformed. Properties priced in the middle quartile of market rents continue to show lower vacancy rates than both the overall market and properties in the top rent quartile.

Multi-Family Rental Vacancy Remains Low, But Segmented By Price Point

Figure 7: National Multi-Family Rental Vacancy Rates by Rent Quartile (Source: CMHC; as of Q4 2025. Q4 = Highest Rent Quartile)

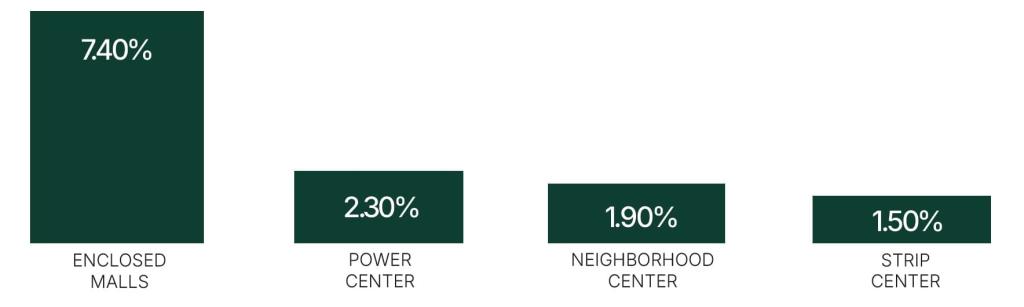

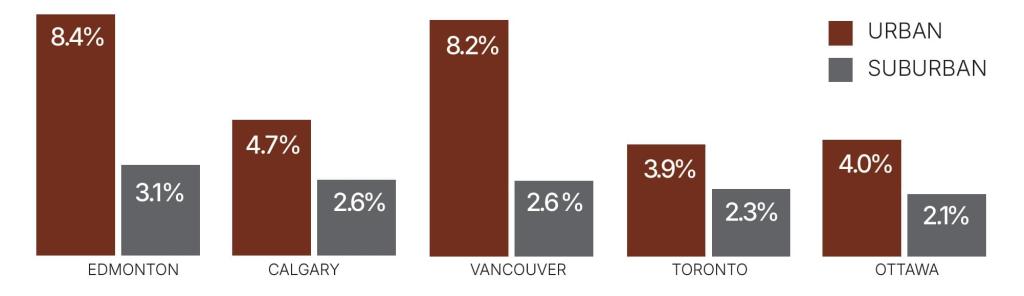

Retail | Stability Within Necessity Driven Formats

Overall vacancy levels remain low across retail segments (Figure 8), though enclosed formats (super-regional and regional malls) continue to see more variability relative to unenclosed formats (power centres, neighbourhood centres, strip centres). Recent closures of major international brands, alongside mixed consumer demand for discretionary retail have been contributing factors. A circumstance of shifting mobility patterns post-pandemic, a ‘core-periphery’ dynamic has also emerged, with suburban retail assets nationally seeing lower vacancies relative to urban assets closer to the financial core (Figure 9).

Strong Relative Performance Among Necessity-Driven Retail Formats In Growing Markets

Figure 8: National Retail Vacancy Rate by Property Type (Source: CoStar, as of Q1 2026)

Figure 9: National Retail Vacancy Rate by Location (Source: CoStar, as of Q1 2026,denotes all retail property types - inclusive of streetfront and mixed-use formats)

Implications

From an investment perspective, this bifurcation across property segments underscores the growing importance of asset selection and a more granular focus on sub-sectors and site-specific fundamentals. Understanding differences in tenant mix, product positioning, amenity profile, and local demand drivers is essential.

A constructive backdrop is that overall vacancy levels in Canada remain comparatively low, reflective of the country’s constrained geography, high barriers to new supply, and structural demand fundamentals. These characteristics continue to provide a degree of resilience across sectors.

Theme 4

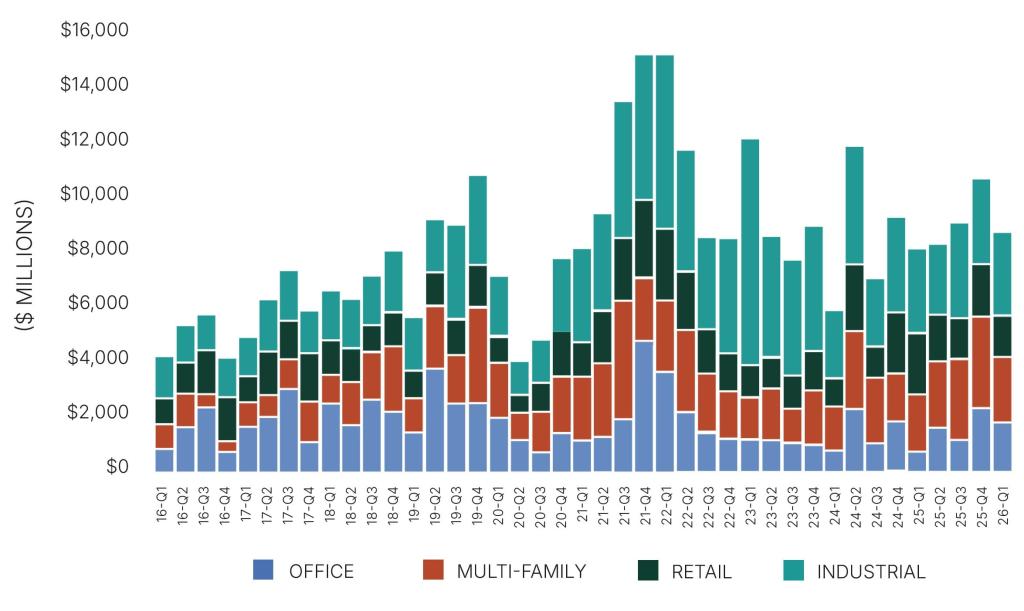

Liquidity Improving, Supported By Larger Portfolio Deals

Overall investment volumes have improved over the past 18-24 months, rising well above post-COVID lows seen through early 2024 (Figure 10). Improvements in deal volume have been broad-based, with all property sectors seeing higher levels of investment activity.

Large portfolio and entity‑level deals have been notable contributors to the recovery and include both multi-property purchases and full/partial interest transfers, alongside firm-level mergers and acquisitions. Between 2024 and 2025, such deals totaled $5.5 billion in Canada, representing 10% of all investment activity. This is compared with just $2.2 billion (2.6% of total volume) during 2021–2022—despite those being record setting years for overall investment activity.

Looking forward, transaction activity should continue to improve, though demand will likely be strongest for assets with stable, predictable cash flow. We also anticipate that the recent pace of portfolio trades, mergers, and co-investments to continue as investors seek ways to deploy capital at scale.

Investment Volumes Generally Up Across All Property Sectors

Figure 10: National Property Investment Volume ($M) (Source: CoStar, denotes transactions $10M+, aggregate of Office, Industrial, Retail and Multi-Family)

Theme 5

Economic And Demographic Shifts Driving A Focus On Regional Differences

The Canadian economy is entering unfamiliar territory as new economic and demographic realities take shape.

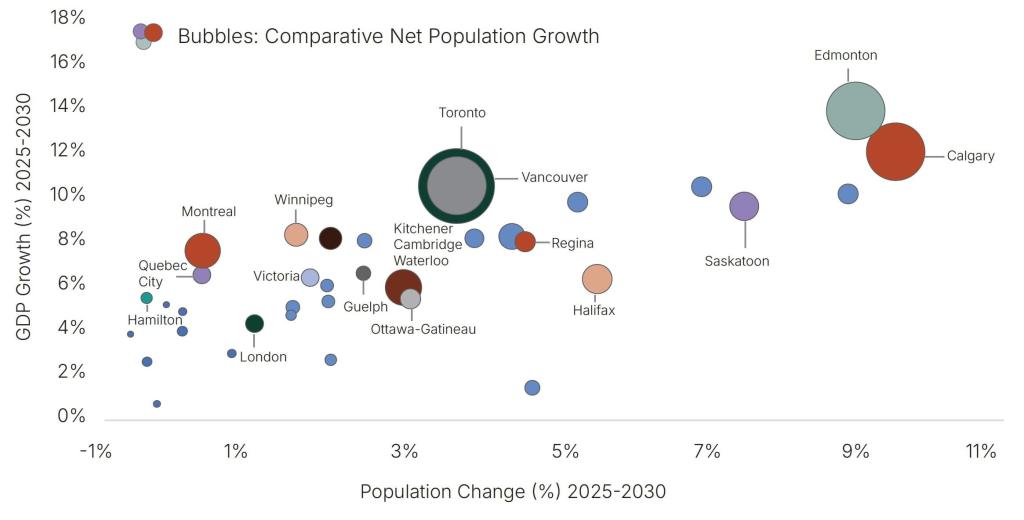

From a demographic standpoint, population growth across major cities is forecast to vary (Figure 11). Unlike the last several years—when record immigration supported broad-based population growth nationally —immigration policy shifts are likely to slow the pace of new entrants to Canada over the near-term. This is expected to amplify competition for people and talent across regions.

From an economic perspective, trade and geopolitical risks continue to create market uncertainty, compounded by their constant evolution —from ‘on-again/off-again’ tariffs, to ongoing and emerging global conflicts.

As for implications, growth is likely to vary across city-regions within Canada. Some markets, however, are better positioned to navigate these risks than others, whether through underlying resilience of their local economies, or through their alignment in industry sectors insulated from—or benefiting by—broader market and economic shifts.

Western Canada—particularly Calgary and Edmonton—is expected to fare well relative to other cities, supported by favourable demographics and Federal investments targeting energy and resource development. Large, diversified cities such as Toronto, Vancouver, and Halifax are also poised for growth on a comparative basis; their broad economic bases provide a level of stability, while sector strengths in financial services, trade, regional distribution, and technology offer a degree of insulation from global risks.

Population And Economic Growth Forecast To Be Segmented Across Major Canadian Cities In Coming Years

Figure 11: Forecasted Net GDP And Population Growth (2025-2030) (Source: Oxford Economics, Select Major Metros Shown)

Conclusions

Overall, it is expected that “bottom-up” approaches to investment strategy, namely a focus on income growth and asset selection will be important for private real estate in 2026. Sectors and assets with below market rents and structural undersupply are best positioned.

A focus on asset selection also increases the importance of sub-sector distinctions and site-specific characteristics. Viewing property sectors simply as “industrial” or “retail” overlooks meaningful differences across property sub-types and locations. Emerging economic and demographics shifts further adds to this dynamic, as property demand is expected to see divergence across regions in coming years.

For more information on attribution analysis see https://www.msci.com/research-and-insights/quick-take/real-estate-asset-selection-drove-performance.

Contact

Anthio Yuen

Vice-President

Investment Strategy & Product Development

Anthio.Yuen@gwlra.com

Madhura Taskar

Analyst

Research & Investment Strategy

Madhura.Taskar@gwlra.com

Disclaimer:

This report is for general information purposes only and is not intended to provide any personalized financial, investment, real estate, legal, accounting, tax, medical or other professional advice. While the information contained in this report is believed to be reliable and accurate at the time of posting, GWL Realty Advisors Inc. and its affiliates (“GWLRA”) does not guarantee, represent or warrant that the information contained on this website is accurate, complete, reliable, verified, error-free or fit for any purpose. No endorsement or approval of any third party or their statements, opinions, information, products, or services is expressed or implied by the contents of this report.

GWLRA expressly disclaims all representations, warranties or conditions, express or implied, statutory or otherwise,

including, without limitation, the warranties and conditions of merchant-able quality and fitness for a particular purpose,

non-infringement, compatibility, timeliness, security or accuracy. The user assumes full responsibility for risk of loss of any

nature what-soever resulting from the use of this report. For more information concerning the terms and conditions of use of

this report, please refer to our website at https://www.gwlrealtyadvisors.com/general-disclaimer.

GWL Realty Advisors Inc. generates value by creating vibrant, sustainable communities that engage, excite and inspire. As a leading Canadian real estate investment advisor, we offer asset management, property management, development and specialized advisory services to pension funds and institutional clients. Our diverse portfolio includes residential, industrial, retail and office properties as well as an active pipeline of new development projects.